|

Author's Note: This article was written and published before the press release with fresh data on the IBS-C trials was published and sent the stock up sharply. (See the first comment below the article for further details.)

From riches to rags

Fallen angels are a value investor classic - and I believe Mr. Market's terrible reaction to the trial results published by Ardelyx (NASDAQ:ARDX) say much more about Mr. Market's irritable nature itself than about the company subject of his irritation. Within one year, Ardelyx at first, based on three interesting promises, was valued as high as $600 million and then crashed down to only $150 million - of which $100 million are net cash. However, two of the initial promises are still intact, as we will see later on.

If you are not familiar with the company, there are a few good overviews of the Ardelyx story here on Seeking Alpha, among which I'd suggest to read first of all the one by IPODesktop to familiarize with the company and its background. Later on, you should also read the trial results I have linked to below to improve your understanding of the subsequent discussion.

What this article will mostly focus on is the company's collaboration with AstraZeneca (NYSE:AZN) and the development of tenapanor for its three potential indications: IBS-C, hyperphosphatemia and albuminuria:

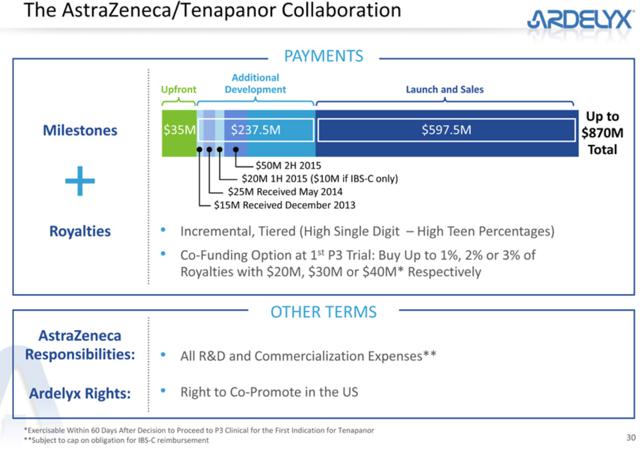

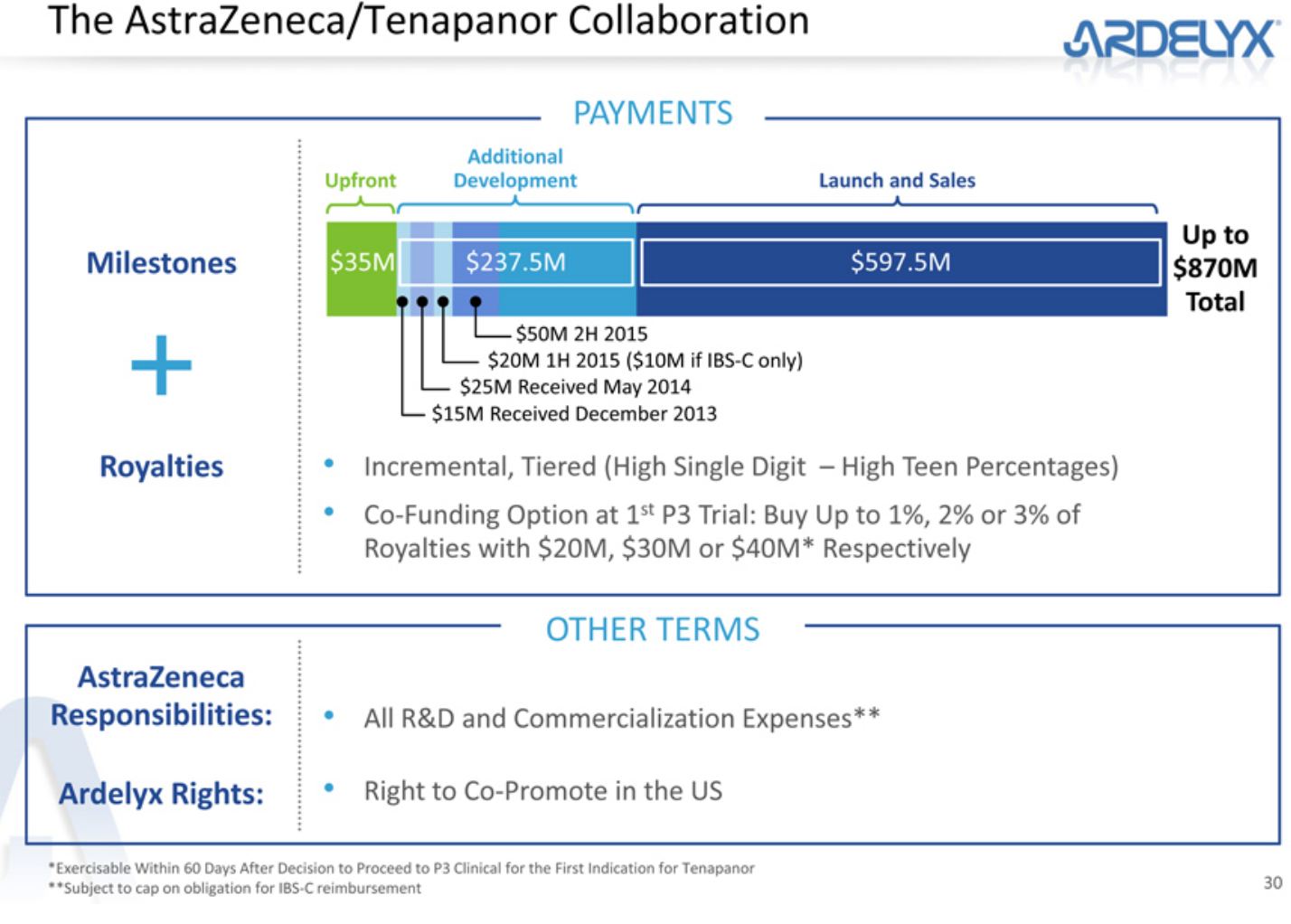

(click to enlarge)

(This and subsequent slides are from a company presentation.)

What we know about the exact terms of this collaboration is what Ardelyx has recently published in its form 10-K:

In October 2012, we entered into a collaboration partnership with AstraZeneca for the development and commercialization of our small molecule NHE3 inhibitors, including tenapanor as well as back-up compounds. […] Under the terms of the agreement, we received a $35.0 million upfront payment and we are eligible to receive up to $237.5 million in development milestones, of which we have received $40.0 million. In addition to the $237.5 million in total development milestones, we are also eligible to receive up to $597.5 million in sales and launch milestones which, when combined with the $35.0 million upfront payment, provides for potential payments of up to $870.0 million. […] We are also eligible to receive incremental tiered royalties based on aggregate annual net sales of each licensed product starting in the high single digits and increasing to high teen percentages as annual net sales increase. If we exercise our right to co-fund the first Phase 3 development program for tenapanor, we could acquire an increase in our royalties by 1%, 2% or 3%. […] AstraZeneca solely funds all development and commercialization costs for licensed compounds and licensed products, except for costs that we elect to undertake if we exercise our right to co-fund certain development efforts in exchange for an increase in the royalty percentage. […]

AstraZeneca has the right to determine which indications it will continue to develop. AstraZeneca has the right to elect to develop one, two or all three of the indications, and AstraZeneca has the right to terminate the agreement upon written notice to us. If AstraZeneca determines that it will advance any one of the indications forward into a Phase 3 clinical trial, we would receive a royalty payment of $50.0 million. In addition, we would receive a $20.0 million development milestone if AstraZeneca determines to move forward with the development of tenapanor by commencing a Phase 2b or Phase 3 clinical study in any of the indications; provided that this milestone payment would be a $10.0 million payment if AstraZeneca decides to move forward with only the IBS-C indication.

We don't know anything about thresholds, quantity and level of any milestone payments beyond the hypothetical $50 million payment for the initiation of a phase 3 study. It seems, however, that milestone payments are already triggered by the advancement of only one of the three potential indications, i.e. Ardelyx should not receive $50 million for every initiation of up to three phase 3 trials, but only one payment for the first phase 3 initiation. This is how milestone payments have been structured so far and it is likely that they will continue this way. On the other hand, the achievement of sales milestones obviously depends on how many horses will be in the race: If only one of the potential indications will be approved, we can presume that less sales milestones will be hit.

The stock market has always been very impressed with the sheer size of the potential payments of up to $870 million (keep in mind that we talk about a company with a market cap of only $166 million), which in my opinion, has somewhat distorted the perception of the source of value in Ardelyx. In fact, as we will see later on, the market seems to believe that Ardelyx' destiny exclusively depends on the continuation of the AstraZeneca collaboration.

At the time of the IPO (June 2014), none of the three tenapanor phase 2 trials had been finished and the market considered Ardelyx like a very promising biotech with three horses in the race. The following chart shows the market reaction to the most important events since then: (click to enlarge) After the IPO at $14, a few sharp moves with relatively high volume stand out: After the IPO at $14, a few sharp moves with relatively high volume stand out:

1. At the beginning of October 2014, the enthusiastic reaction to positive phase 2 results for the IBS-C (irritable bowel syndrome with constipation) indication brought the stock to $21.

2. Mid-December 2014, a sell-off which was probably caused by the expiry of the lock-up period following the company's IPO in June. From its ATH of $35, the stock halved in a few weeks.

3. As this obviously had nothing to do with Ardelyx' fundamental value, the stock market quickly recovered half of the December losses. But then, at the beginning of February 2015, another sharp sell-off was caused by a surprisingly high percentage of patients with diarrhea in the phase 2 trial for the ESRD hyperphosphatemia indication. Afterwards the stock was back at its IPO price.

4. The last sell-off down to $8 came a few weeks ago, when Ardelyx reported that the phase 2 trial for tenapanor's third and last potential indication did not meet its primary endpoint. The company is now priced at an EV of only $66 million, indicating that Mr. Market does not expect further milestone payments and has already written off the AstraZeneca collaboration for all three indications.

So Mr. Market was extremely pleased with this business after the first trial (1) and started to get a bit worried (2) already before the expiry of the lock-up period. (The sell-off started one day early.) At point (3) Mr. Market definitely lost his calm with Ardelyx and (4) represented just the final confirmation for the pessimists. But most of the pessimists had already lost their patience before, hence, most interestingly, the event did not manage to move as much volume as the previous two trial results despite being objectively the worst and only definitive hit to part of the company's hopes.

What I want to underscore here is that the case for the IBS-C indication is still absolutely intact, while for the hyperphosphatemia indication there is still hope. The only indication that certainly won't be pursued anymore is the one under point (4).

In fact, the company stated in its Q1/15 press release:

In June, Ardelyx is scheduled to have an End of Phase 2 meeting with the Food and Drug Administration (FDA) in order to obtain agreement on pivotal study designs, and safety and efficacy endpoints for Phase 3 studies for tenapanor to treat IBS-C.

Ardelyx is preparing for the continuation of the development of tenapanor under a variety of scenarios, and intends to be in a position to initiate a Phase 3 clinical program for tenapanor in IBS-C in the fourth quarter of 2015 and to continue the development of tenapanor for the treatment of hyperphosphatemia in CKD patients on dialysis, should it regain the worldwide rights to the program.

This means that, even if AstraZeneca should decide to stop the cooperation on the two remaining indications altogether and give the tenapanor program back to Ardelyx, the company would either search for a new partner or continue on its own. With $100 million of cash, this is certainly a possibility. And it also means that in the opinion of Ardelyx' management, the potential returns warrant such an investment. Considering that the CEO comes from Genzyme, where he was involved in the launch of today's market-leading phosphate binder Renvela, he probably knows what he is talking about.

In my opinion, given the favorable outcome of the IBS-C trial (which had even Mr. Market's enthusiastic approval), there are no reasons for AstraZeneca to stop developing tenapanor for this indication, while there is a chance that the British pharma giant might stop developing the drug for hyperphosphatemia. In this case, Ardelyx would still receive milestone payments of $10 million for the conclusion of the IBS-C study and $50 million for the initiation of the phase 3 trial for this indication, i.e. under the assumption that the stock remains where it currently stands, the company would trade for an EV of close to zero. This confirms what I said before, i.e. that the market seems to discount that AstraZeneca will drop tenapanor for all indications.

A final consideration on the trials: All healthcare investors should know that phase 2 trials are the toughest. On average, only ~35% of phase 2 trials are successful. This means that, on a probabilistic basis, right after the IPO, Mr. Market could count on 1 successful trial out of the 3 potential tenapanor indications. If we count the hyperphosphatemia trial as a 50% success, Ardelyx effectively delivered one and a half successes in three trials. Hence, if the IPO price was fair, today the market should value the business at least as highly. Yet it trades at a 30% discount. And if the market price after the first trial results was fair, there is a strong argument for a similar price today - because, on a probabilistic basis, after the first one had been concluded successfully, the two remaining were worth 0.7 successful trials and Ardelyx delivered 0.5.

Finally, as we will see below, the successful IBS-C indication is certainly one of the most valuable, while the unsuccessful indication was considered as the toughest hurdle. We will also see that Mr. Market was probably about right with his valuation before his diarrhea phobia made him lose his temper.

Tails I win, heads I don't lose anything

To understand the two possible outcomes that investors in Ardelyx will face over the next five weeks (AstraZeneca will have to communicate its decisions on or before June 29, 2015), I have to dig a little deeper. First of all, let's try to understand the potential of the two indications under discussion.

Hyperphosphatemia

The total, global size of the phosphate binder market for ESRD patients is expected to reach $2.3 billion within the next 5 years.

The following information is taken from the 2014 10-K:

Limitations of current products for hyperphosphatemia

Since dialysis is unable to efficiently eliminate excess phosphorus, CKD-5D patients are put on restrictive low phosphorus diets and are prescribed medications called phosphate binders, the only pharmacologic interventions currently marketed for the treatment of hyperphosphatemia. Phosphate binders are a collection of drugs whose function is to bind, or absorb, dietary phosphorus and are taken in conjunction with meals and snacks. They include calcium, iron or lanthanum, a rare-earth metal, which bind to and precipitate with dietary phosphate in the GI tract. The goal is for patients to eliminate the precipitated phosphorus in their stool. A limitation of this approach is the systemic excess absorption of calcium, iron or lanthanum, resulting in side effects and other unintended consequences for CKD-5D patients. In an effort to eliminate these unwanted side effects, non-absorbed exchange resins, such as sevelamer were developed to bind to phosphate in the GI tract and to be eliminated in stool.

Safety and tolerability have been significant concerns with many approved phosphate binders. The more common side effects of approved phosphate binders include long-term vascular calcification, nausea and vomiting, diarrhea or constipation and ileus or disruption of the normal propulsive ability of the GI tract. CKD-5D patients take on average 10-14 oral medications each day, and they are severely restricted in their fluid intake. In addition, to control their serum phosphorus, their phosphate binder-related pill burden is significant, typically consisting of nine or more pills a day. The amount of phosphate a binder can remove is limited by its binding capacity, and therefore, increasing the dose, and the pill burden, of the binder is the only way to increase the amount of phosphate being bound and excreted. As a result, prescribed binder doses are intolerable for many patients.

The effectiveness of current treatment with phosphate binders is limited. For example, in a 2012 study conducted by Amgen in 1,430 ESRD patients on hemodialysis in the United States in which 89% of the patients in the study had previously been prescribed phosphate binders, the average baseline serum phosphorus level was 6.4 mg/dL, significantly above the target for dialysis patients of 5.5 mg/dL and far above normal serum phosphorus levels of 2.6 to 3.8 mg/dL.

Other studies suggest that this lack of efficacy is due primarily to poor patient compliance associated with significant pill burden and other tolerability issues.

Tenapanor's competitive advantage in hyperphosphatemia

Given that the objective is to lower serum phosphorus levels to below 5.5 mg/dL in dialysis patients, and that many of these patients are unable to accomplish this goal with currently marketed phosphate binders, there is a clear medical need for new treatments for hyperphosphatemia. We believe that there is a significant opportunity for new agents with new mechanisms, demonstrated efficacy, a strong safety profile, and significantly lower pill burden. We believe that tenapanor, if approved, has the potential to have the lowest pill burden among any of the marketed hyperphosphatemia drugs, with milligram rather than gram quantities dosed once or twice daily.

Now, the trial results for this indication obviously were a mixed bag. While the potential to have the lowest pill burden among phosphate binders is still intact and the drug effectively reduced serum phosphorus with very low dosing, the high percentage of patients complaining about diarrhea could kill the drug. Diarrhea is a common problem with phosphate binders (normally about 20% of patients report this adverse event), but tenapanor had a rate of close to 50% in the 10 mg BID dosage group (which is the dosage the company wants to test in a potential phase 3 trial).

Based on positive physician feedback and the still remaining possibility to cover an unmet medical need for at least part of the ESRD population, the company is determined to move the drug forward nevertheless. However, as far as the sales potential is concerned, I would cautiously estimate a sales potential of only $300 million for tenapanor (~13% market share).

IBS-C

Size of the IBS-C market

Based on reports in the literature regarding the prevalence of IBS in the U.S. population and the percentage of individuals who have IBS-C as opposed to other forms of IBS, we estimate that approximately 1.4% of the U.S. population has IBS-C, or about 4.4 million individuals. Of those, approximately 1.0 million patients have been diagnosed with IBS-C. Additionally, there are about 6.6 million IBS-C patients in Europe and about 3.4 million in Japan.

The per-patient economic burden of IBS-C is estimated to be $1,500 to $7,500 per year in direct costs and $800 to $7,700 per year in indirect costs, implying the total burden in the United States is $2 billion to $15 billion.

Limitations of current products for IBS-C

Numerous treatments exist for the constipation component of IBS-C, many of which are over-the-counter. We are aware of two prescription products marketed for IBS-C, Linzess (linaclotide) marketed by Ironwood Pharmaceuticals and Actavis and Amitiza (lubiprostone) marketed by Sucampo and Takeda. In Phase 3 clinical trials of Linzess in IBS-C patients, up to 19.8% more patients receiving Linzess than placebo reached the primary endpoint, overall responder rate, indicating a significant response during 6 out of 12 weeks of treatment. In these studies, Linzess caused diarrhea in up to 20% more patients than placebo.

Tenapanor's competitive advantage in IBS-C

We believe that tenapanor may offer a significant benefit over currently marketed drugs like Amitiza and Linzess, due in part, to the potential to adjust the dose and/or dose frequency of tenapanor in order to optimize its efficacy and minimize diarrhea. The data we have generated in both animal and human studies have suggested that the effect of tenapanor for the treatment of IBS-C can be modulated by adjusting its dose and dose frequency. […] Our phase 2b clinical trial demonstrated a stronger efficacy signal than the Phase 2a with a low to moderate rate of diarrhea of 11.2% versus placebo. Given that we have observed a gradual dose response of sodium with increased dose and dose frequency of tenapanor and that diarrhea represents an exaggerated pharmacological response to the drug, we believe it may be possible to start: dosing at once daily and/or a low dose. Those who do not respond would receive a higher dose or increased dose frequency. This ability to titrate the dose of tenapanor, if proven in subsequent clinical trials in IBS-C patients, would represent a significant differentiation of tenapanor versus currently commercialized products, and may allow optimization of dose response while limiting diarrhea.

So the case for the IBS-C indication is still 100% intact. There seems to be no reason for AstraZeneca to discontinue its development. Even the rate of diarrhea seems to be acceptable and much lower than in other IBS-C drugs.

For me, it is actually quite astonishing to see Mr. Market presuming that the AstraZeneca collaboration will be 100% terminated just because of undesired side effects in one of the three indications and an unsuccessful trial of another one. After all, while diarrhea is certainly an ugly side effect for already debilitated ESRD patients that usually have multiple co-morbidities, in constipated IBS patients it is almost desirable. Certainly it is of much less concern. What the market is confused about here is probably how the very same molecule can result in a comparatively much worse diarrhea rate in ESRD patients and, at the same time, in a much better diarrhea rate in IBS-C patients. It seems to be hard to believe that tenapanor could have a competitive advantage based on its low rate of diarrhea in IBS-C patients after the subsequent hyperphosphatemia trial. So Mr. Market seems to have developed some kind of diarrhea phobia and totally ignores that the two patient populations are of very different nature: IBS-C patients are of average health, while ESRD patients have an average life expectation of only 4 years. They have to respect an extremely strict diet, hence don't assume food and beverages like everybody else. Usually they have multiple other health issues and take lots of drugs. Hence, the extremely different results from the very same molecule should not be as surprising.

Anyway, based on the trial results, in the case of IBS-C AstraZeneca and Ardelyx don't have anything to worry about. The trial was successful and the drug seems to have great potential. In fact, the two mentioned competitors, Linzess and Amitiza, are forecasted to rake in sales of ~$400-500 million each in 2015 (globally) and are still growing strongly. As tenapanor could well prove to be superior to these drugs, I would pencil in potential sales of at least $500 million.

Valuation

The valuation of development stage biotechs is always tricky. Even more so, if not only we have to consider the probability of success for the various early stage assets, but also the probability of continuation of a development collaboration that could substantially alter the equation. Finally, in this case, the structure of future milestone payments is not at all clear.

To provide an example of the intricate nature of this exercise, I will start with the bear case or "Heads" scenario:

If Ardelyx moves ahead on its own with both indications

Based on the trial results, I would see this as pretty unlikely and assign a 20% probability to such a scenario. How it would play out is not clearly predictable, as the company might simply find a different partner, pay for phase 3 on its own and then find a partner, or find different paths for each of the indications. Moreover, if the company covers development, future royalties should be higher - but only if it manages to find a partner that accepts such a deal. Otherwise Ardelyx might even end up building its own sales team in the U.S. (which would lead to high costs) and accepting a not ideal partnership in other parts of the world (and thus wasting some of the drugs' potential). Finally, Ardelyx might also be forced to raise additional capital and dilute shareholders. On the other hand, as some analysts point out, a return of the whole tenapanor program to Ardelyx might even represent an opportunity for higher results, as the company could enjoy a higher percentage of the potential profits despite the fact that large part of the trials have already been paid by AstraZeneca.

Bottom line: this scenario is certainly worth something, but it is impossible to estimate precisely how much. Therefore, I would settle for the absolute minimum which I define as a quarter of the best case scenario. This is probably overly cautious because there would be excellent arguments to raise estimates for the IBS-C drug, if it was 100% owned by Ardelyx. Moreover, even after a hypothetical termination of the AstraZeneca collaboration, a new partner might be around the corner. However, just for the sake of caution, let's presume that the tenapanor asset without AstraZeneca is worth only 25% of what it could be worth with the partnership. So its contribution to the total, probability-weighted valuation will be 20% of 25%, i.e. only 5% of the best case scenario.

If AstraZeneca progresses one or two indications to phase 3

In this scenario, we need to consider the different chances of the two remaining indications. While I consider the IBS-C indication a certainty, I believe that the hyperphosphatemia indication only has a 50% chance. This translates into the following best case valuation:

IBS-C

Immediate (i.e. within 2015) milestone payments: $60 million

Sales potential 7 years from now: $500 million

Probability of approval: 50% (i.e. a roughly average approval chance for phase 3 drugs)

Probability weighted sales potential: $250 million

Resulting royalties to Ardelyx: ~$30 million

Value of these royalties in 2022 at a conservative multiple of 10: ~300 million

NPV of these royalties (discounted at 15%): ~$115 million

Future milestones (estimated, one third of remaining milestone payments after the immediate ones): ~$240 million

After accounting for 50% probability of approval: ~$120 million

NPV of these milestones (discounted at 15% over an average period of 3.5 years): ~$74 million

Total NPV for IBS-C: $249 million (60 + 115 + 74)

One might argue here that I have applied the 50% approval probability to the future milestone payments despite the fact that they certainly include milestones payable before approval. However, I prefer to be cautious here, because the overall structure of the payments is unknown.

Hyperphosphatemia

Immediate (i.e. within 2015) milestone payments: $10 million

Sales potential 7 years from now: $300 million

Probability of approval: 33% (i.e. a below average approval chance for phase 3 drugs)

Probability weighted sales potential: $100 million

Resulting royalties to Ardelyx: ~$12 million

Value of these royalties in 2022 at a conservative multiple of 10: ~120 million

NPV of these royalties (discounted at 15%): ~$45 million

Future milestones (estimated, one third of remaining milestone payments after the immediate ones): ~$240 million

After accounting for 33% probability of approval: ~$79 million

NPV of these milestones (discounted at 15% over an average period of 3.5 years): ~$48.5 million

Total NPV: $103.5 million (10 + 45 + 48.5)

Resulting NPV for hyperphosphatemia after 50% reduction: ~$52 million

TOTAL value of best case scenario: $301 million (249+52)

We can now assemble our probability-weighted total valuation for the company (exclusive of net cash):

20% of worst case "Heads" scenario, which I have defined as 25% of the best case: $15 million (0.2 x 0.25 x 301)

80% of the best case "Tails" scenario: $241 million (301 x 0.8)

TOTAL: $256 million

Inclusive of net cash (+$100 million): $356 million

However, we are not done yet. There is some additional value in Ardelyx that will remain in both scenarios.

What remains in both cases

In addition to the more or less enthusing NPV of the tenapanor story, the current EV of ~$66 million also buys you what follows:

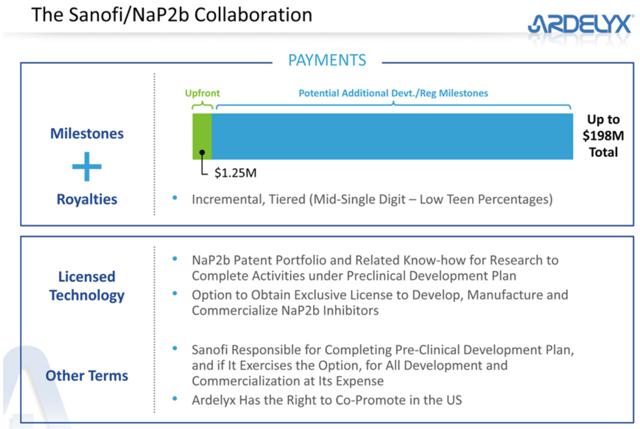

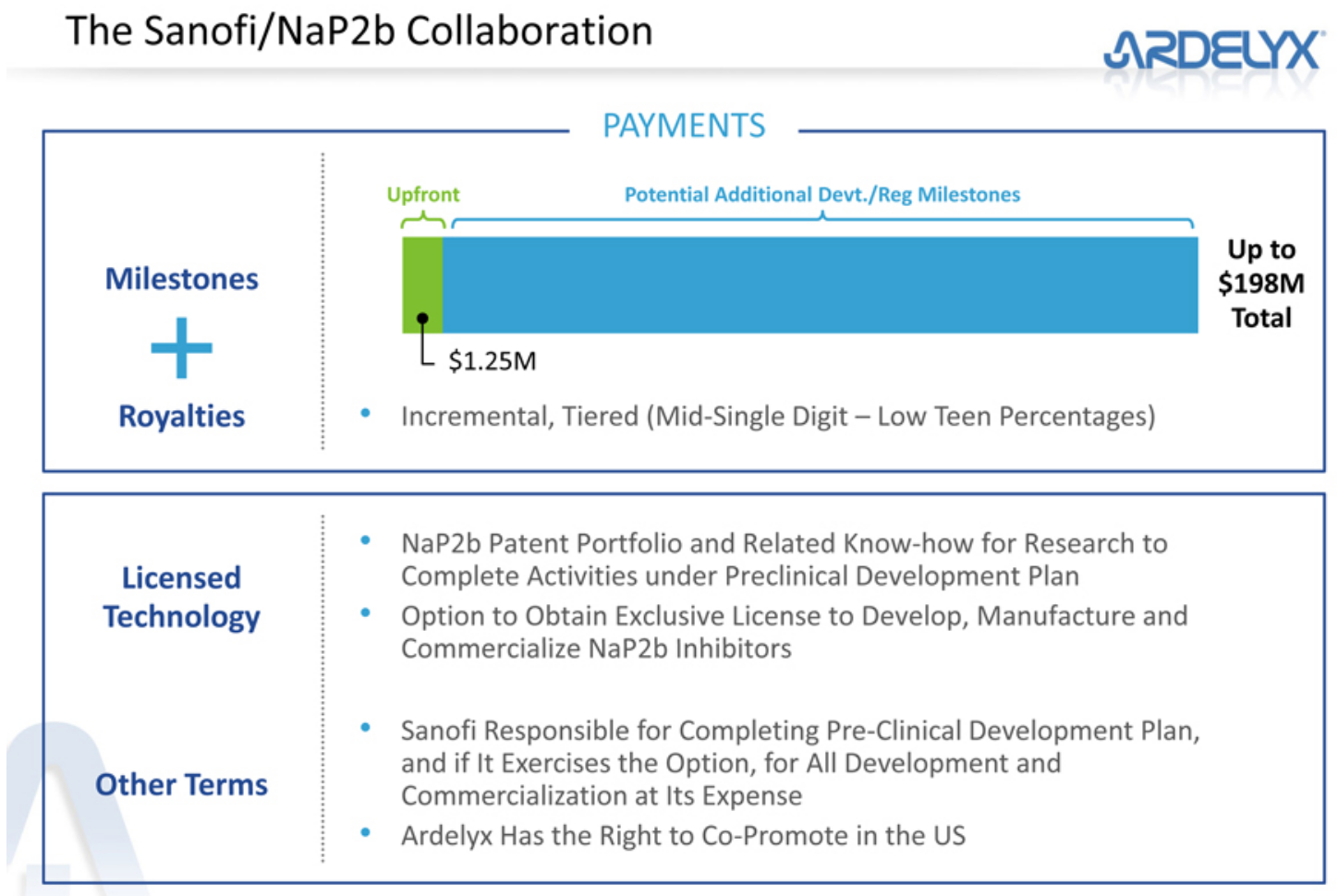

- The Sanofi collaboration with potential milestone payments of up to $198 million and future royalties.

(click to enlarge)

NaP2b is an intestinal phosphate transporter whose activity is believed to account for a significant portion of dietary phosphate absorption in humans. We believe the inhibition of NaP2b would provide utility for the treatment of hyperphosphatemia in CKD-5D patients. We have identified several NaP2b inhibitors that showed activity in vitro and in animal models. In rats with normal renal function, certain NaP2b compounds were able to reduce urinary excretion of phosphorus better than commercial phosphate binders such as sevelamer or colestilan, even when these compounds were dosed at approximately 1/10 of the dose of the commercial binders. In addition, our NaP2b compounds had additive effects when administered with sevelamer or colestilan. […]

We have shown that our inhibitors are able to inhibit phosphate regardless of the amount of phosphate in the diet. We believe this mechanism would have a significant advantage over phosphate binders, and may allow us to significantly decrease pill burden while retaining a similar phosphorus effect. Additionally, we believe that the use of a NaP2b inhibitor in combination with a phosphate binder may allow the dose of the phosphate binder to be reduced.

(Source: 2014 annual report)

As Sanofi's market leading phosphate binder Renvela/Renagel will soon face generic competition, the French giant deeply needs to innovate and Ardelyx' NaP2b inhibitors could significantly improve patient experience, adherence and efficacy by reducing the pill burden by a factor of 10.

- a pipeline of several development candidates

- a top notch management that has managed to keep the annual cash burn rate below $20 million and has among its top priorities to avoid shareholder dilution. (click to enlarge)

By the way, shareholder interests appear to be well aligned, with management holding ~6% of shares outstanding and the founding venture capital funds NEA and CMEA still holding over 50%.

Let's be ultra-conservative and assign to these additional assets a value of zero.

Conclusion

According to our calculation, the probability-weighted value of Ardelyx is $256 million + net cash of about $100 million, i.e. a total of $356 million or ~$19 per share, indicating an upside of over 100%.

$19 is also approximately the average trading price of the stock since its IPO - perhaps demonstrating that over longer stretches of time Mr. Market can be quite efficient (when he is not irritated by diarrhea phobia).

It is also good to see that at the present price level we do not really need the contribution from the complicated and very roughly calculated worst case scenario, as even if we put its contribution to zero, the shares should still trade for almost twice the current share price.

We also don't really need the hyperphosphatemia indication, as the IBS-C indication alone easily justifies an investment.

Now, this is obviously entirely based on probabilistic calculations and everybody should know that even tall guys can drown in a river that on average is only 50 inches deep. So let's consider the troughs and peaks as well:

If AstraZeneca continues to develop tenapanor for at least the IBS-C indication, Ardelyx would be worth $249 million (100% of the IBS-C best case scenario) + net cash of $100 million, i.e. a total of $349 million or ~19 per share, even if no additional indication is pursued by Ardelyx itself.

If the Brits continue the development of the other indication as well, we can add 100% of the hyperphosphatemia best case scenario, i.e. another $103 million, for a combined total value of ~$24 per share.

On the contrary, if Ardelyx develops both drugs on its own, it does not require heroic assumptions to justify the current market cap: $100 million of cash are worth $100 million. Add a few million for the Sanofi collaboration, a mere $40-50 million for the (sharply reduced) potential future returns of tenapanor and something for the pipeline - and we are already close to the current capitalization of $166 million.

As I said before, not all analysts see the potential return of the tenapanor program from AstraZeneca as a catastrophe for Ardelyx. Some even believe the IBS-C program would be worth more, if the company regained all rights - which makes me feel even more comfortable with the virtually non-existent downside.

Disclosure:The author is long ARDX. (More...)The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it (other than from Seeking Alpha). The author has no business relationship with any company whose stock is mentioned in this article.

|

Log in to explore the world's most comprehensive database of dialysis centres for free!

Log in to explore the world's most comprehensive database of dialysis centres for free!

INDEPENDENT MEDIA

Kidney patients seeking dialysis at Addington Hospital have had their time on the dialysis machines cut by half. Photo: S'bonelo Ngcobo

INDEPENDENT MEDIA

Kidney patients seeking dialysis at Addington Hospital have had their time on the dialysis machines cut by half. Photo: S'bonelo Ngcobo